This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

Login with your ZeroHedge Premium account

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

JPM's Kolanovic strikes again;

1, low rates leads to institutions rotating out of bonds into equities

2, creates downward pressure on volatility

3, which in turn creates a positive feedback loop where systematic and disc hedge fund strategies increase allocations to equities (this could play put for most of 2021)

4, if current below average exposure goes to historic percentile would result in $550 bn inflow from systemic and hedge fund strategies

5, add forgotten buybacks to the mix and Kolanovic argues for their 4400 SPX px target.

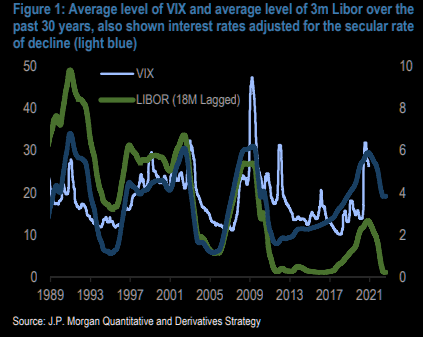

Below chart shows that average VIX levels closely follow levels of interest rates with a ~18-month lag. Conclusion is basically;

"Given the significant increase of monetary accommodation 9 months ago, we expect it to pressure volatility for most of 2021"

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

This article is part of our Premium coverage, please click here to login and access it or sign up for a Premium account.

Probably the Most Bearish Chart of the Weekend

Three Crosscurrents Reshaping Markets

The AI Trade Is Coming Apart

Bond Volatility Is Sending A Warning

What If The Bond Market Is Right About AI?

Oil's Next Move Hinges On Three Variables

The Market Is Starting To Crack

Inside The Magnificent 7 Selloff

The Dominoes Are Starting To Fall

The Complacency Trap

The Oil Time Bomb: How To Play It

One Of These Markets Is Wrong

Semis Bounced. Don't Celebrate Yet.

Why Wall Street May Be Too Bearish On The Mag-7

The Next AI Arms Race Is Being Fought In Nuclear

The Market's Most Dangerous Bet

Europe's Biggest Risk Is Back - And Nobody Seems To Care

Cloud Re-Accelerating. Security Software Up 100% In 3 Months. Apple At 11x Sales

Everyone Gave Up On Silver

Oil Bears Just Got Steamrolled

The Bond Market Is Far Too Complacent

The Gold Squeeze Nobody Sees Coming

The Gold Squeeze Nobody Sees Coming

The Forgotten Trades Strike Back

Europe Is The Surprising Winner Of The Summer

What Normally Happens After A 20% Drawdown In Semis?

The Cracks Beneath The Surface

Calm Before The Storm? The VIX Isn't Telling The Whole Story

The AI Trade Is Rotating To China

The AI Trade Has A Leverage Problem

"Your Gross Is Your Net"

Does Gold "Have" To Trade Down To $3500 To Make A Bottom?

The Amateurs Are Buying Tech While The Pros—and The Insiders—Are Selling

Fastest and Deepest Tech MoMo Sell-Off in History

Semis Positioning Still Close To Highs

Has The Bar Been Raised Too High?

The Perfect Storm: Everything That Could Go Wrong... Just Did

The Whole Market Is One Trade

The AI Golden Child Is Finally Bleeding

Check These Seven Charts Before You Take Vacation

Is Spain Secretly The Best Country In Europe?

One Of Wall Street's Biggest Winners... And Most Hated Trades

The Volatility of the Momentum Factor is Extremally High Now

When Credit Stops Believing

Who's Buying, Who's Selling? The Latest Signals From Wall Street

Semiconductor Supercycle Rolling Over?

ChatGPT Killed America

The AI Ponzi Machine Is Getting More Sophisticated

The Usual Suspects Didn't Go "Dracarys" Last Night in Paris (Only in London and Amsterdam)

First Signs of a Sentiment Change in Bitcoin

Hyperventilating About Hyperscalers

Five Charts That Matter This Wednesday

Dubai's Ground Zero

AI Under Attack

What About 2027?

The Top 1% Owns America

The Macro Strategist's Case For Owning Emerging Markets

Five Charts That Matter

Never Bet Against America

The Most Hated High Ever?

The End of the Affair

Forget Property: China Has Picked Its New Growth Engine

Pointing Out The Ones Nobody Likes

The AI Volatility Monster

The Forgotten Metal Is Waking Up

The Leaders Are Breaking

The AI Memory Trade Is Unraveling

In Sickness And In Health

Time For Gold?

The AI Feedback Loop Is Reversing

What We Witness Now Has Only Ever Occurred At Major Turning Points

The Market Is Starting To Shift

Mania Made In Korea

Software Strikes Back

AI: When Scarcity Becomes Abundance

Bond Vol Is Stirring

Bitcoin: Broken, Or Bottoming?

Go Woke Go Broke: Nike Stopped Obsessing Over Athletes And Started Obsessing Over Activism

Sell Low, Buy High

Too Much Big Tech Fear?

China's Forgotten Giants

Our Favourite Goldman Indicator Is Back: Now The Most Stretched Since 2024

7 Magnificent Reasons To Buy Magnificent Seven

The Bounce

The Sentiment Split

Remember Software?

Always Something To Chase

Time For Tech?

The Insane Earnings MoMo Losing A Little MoJo

The AI Trade Is Eating Itself

"I drink your milkshake! I drink it up!"

The AI Trade Is Getting Complicated

The China Washout

The AI Trade's Inflection Point

The World's Biggest AI Pressure Cooker

The AI Apocalypse: From "Don't Panic" To "15 Million Job-Body-bags"

The End Of The MAG7 Trade?

When Leverage Becomes The Market

Silver's Great Implosion

Gold Isn't Trading Like Gold Anymore

The Liquidity Crime Scene: Follow The Money

Crowded. Leveraged. Extended.

Emerging Markets Or AI Mania?

The Dollar Is Dead. Long Live The Dollar

Pressure Building In Semis

The Dollar Has A Message For AI Bulls

Imagine VIX At 95

Biotech Breaks Out As Pharma Starts Looking Past 2031

The Number Of Things That Need To Go Right

The Dollar Breakout Nobody Believed

The AI Trade Is Getting Uncomfortable

The World's Biggest Trade Starts To Crack

Gravity Strikes The Asian AI Casino

Lag7

1995 Or 2000?

Gold's Next Big Move

The Great AI Divergence

Too Big To Ignore

You Think The Hyperscalers Have Too Much Power Already?

Welcome To The Ultimate K-Shape

Panic Buying: Hedge Fund Leverage At 4-Year Highs After One Of The Sharpest Buying Periods In History

Something Doesn't Add Up

The Great Concentration

The Rise Of AAMON

Netflix & Spotify Under Attack

Bigger Than Dot-Com

Goldman's Tactical Capitulation Is Your Buy Signal

The Daily Wrap

China AI: What If Good Enough Wins?

The Post-Modern World: Why The Winners Of The Next Decade May Look Nothing Like The Winners Of The Last One

Semis: The New Systemic Risk

The Dollar Trigger

Something Doesn't Add Up

Everyone Fears Inflation. Bond Vol Doesn't.

The Bubble Nobody Calls A Bubble

The AI Beast Inside EEM

What Is Happening To IT Budgets In The Age Of AI?

Bubble Charts >> Bullish Charts

Semis Dropped 6%. Is The Momentum Party Over?

The Mania Monitor

What If The Oil Market Is Wrong?

The Calm Before Volatility?

The Leverage Casino

The Gold Powder Keg

Who The Hell Is Doing All The Buying?

Musk Winning On All Fronts: Deliveries Tracking Ahead of Consensus

The Risk-On Machine

The Tech Volatility Anomaly

The Most Important Chart In Semis

The Silver Bear Trap

The Max Frustration Market

Peace Deal Panic: What If The Bulls Were Right All Along?

Tech: 99th Percentile Longs Meet 99th Percentile Volatility

I Love You, You Pay My Rent: The Most Expensive Bromance In Markets

Private Credit Is Supposed To Be Cracking. So Why Does Nobody Seem To Be Selling?

The Bounce Changes Nothing

Oil Bulls Have Disappeared

One Market Is Lying

That Was Quick: Hedge Funds Just Flushed Positioning Back To The 8th Percentile

This Is What A Broken Market Looks Like

The Two-Way Panic Market

Silver - Back From The Dead?

Have No Fear, Says The Cat In The Hat (And Goldman Sachs)

The Great Debasement Unwind

The AI Boom Is Becoming A Volatility Story

Software's Second Chance

The AI Proxy Nobody Realized They Owned

The Fragile Market

Is long Financials the ultimate hedge for the AI trade?

This Still Isn't Panic

The Hyperscaler Capex Just Keeps Getting Bigger And Bigger

Born Rich, Stay Rich

Funding The AI Mania

If Gold Can't Rally Now, When Can It?

The ETF Casino Is Running The AI Trade

Nobody In Control

The Rally's Biggest Buyer Could Become The Next Crash's Biggest Seller

Cracks In The AI Casino

What Does Silver Know?

Don't Trust The Bounce

Why Isn't The Dollar Higher?

The Bounce Trap

Mallmaxxing, Millionaires And The Myth Of The Broke Consumer

The Hidden Inflation Story Nobody Is Watching

The Most Important SOX Chart Right Now

The AI Trade's Fragility Problem

Ron Baron Sees $30 Trillion, Revolut Is Pitching SpaceX To Seventh Graders...

The Dip-Buyers' Survival Guide

The Curious Case Of The Bearish Bull Market In Gold

The AI Trade Just Hit A Wall

The AI Trade Just Hit A Wall

Leveragepalooza: Sell, Sell or Sell

Bloodbath

Fear Returns To Wall Street

Semis Slaughtered

Red Alert For AI Bulls

The First Crack In The AI Mania?

The Ghost Of 2000 Just Called — It Wants Its Bubble Back

Several Markets Are About To Decide

Has Everyone Given Up On Gold?

The Bond Market Holds The Key

From SOX To MAG?

Hedging Downside Risks Via Put Spreads Makes Sense In Our View

The First Cracks

Bitcoin's Moment Of Truth

3 Mega-Cap Charts We Are Watching

May The Deals Be With You

The Margin For Error Is Shrinking

Emerging Markets Rally Broadens Beyond the Semiconductor Boom

The Market Has Forgotten How To Go Down

Oil Up. Rates Up. Stocks Don't Care.

Investors Are Looking At The Wrong AI Chart

The Year The Magnificent Seven Stopped Being Magnificent

The IPO Market Is Back. Investors Should Remember What Usually Happens Next

The IPO Market Is Back. Investors Should Remember What Usually Happens Next

More AI, No Protection

Nobody Wants Protection

The Most Speculative Market On Earth

The Most Underowned Trade In Global Tech Is Starting To Move

Nobody Wanted Software. Now Everybody Does.

Every Bulldog Apparently Has Its Day: Goldman Says Buy Britain

Perfection Prevails

The Trade Everyone Missed

Nobody Wants Bitcoin

Speculation Nation

Nobody Wants NVDA

Europe: Burning In The Streets, Underowned In The Books

Ford Flying, Materials Moving & Some Real Early-Cycle Optimism

The 6 Tech Charts That Just Need Bigger Charts

10 Charts That Make Us Go Hmmm...

The Semiconductor Boom Keeps Finding New Gear

SaaSmageddon Canceled: Software Stocks Rip For Seven Straight Weeks

Everyone Is Long. What Could Possibly Go Wrong?

What If Everyone Is Wrong And SpaceX Is Actually A Great Short?

Nobody Wants Protection. Nobody Wants Gold. Nobody Wants Software.

The Strongest Buyer Never Stopped Buying Gold

Everybody Loves Semis. Nobody Loves Software.

Another Rates Breakout Just Died

The Market Is Now Panicking Not To Panic

Who's Going To Change Grandma's Diaper?

1997 With GPUs

Max Pain

Housing Taking An Extended Ride On The Flatline

The AI Trade On Steroids Is Wobbling

Semis Killed Bitcoin

The “Most Fundamental Rally Ever” Is Breaking With Fundamentals

Kalshi Ate Robinhood’s Lunch

The Return of “Higher for Longer”

The Melt-Up Still Owns The Trend But The Upside Reflex Is Fading

Semis Leverage Machine Starting To Wobble?

AI Stole Gold’s Story

The Korea AI Mania Is Entering Air Pocket Territory

Enfeebled Europe Closing in on ATHs

In Semis We Trust

Semis Officially In Full Panic-Buying Mode

The Semiconductor Boom Is Starting To Look Like Dutch Disease

Head Fake Or Next Leg Higher In Rates?

The Most Hated Trade On The Screen May Be About To Rip Again

AI Melt-Up Bubble? Maybe. Earnings Explosion? Definitely

Sold The Downtick

The Melt-Up Machine

Can’t Spell China Without AI

Trickle-Down Economics Just Bought Another Yacht

The Most Hated ATH Ever - And Now With Ceasefire Catalyst

One Trade To Rule Them All

Ozempic Was The Warm-Up. RETA Is The Killer

Nobody Fears Downside Anymore

Wall Street Is Panic Buying Upside As Protection Collapses

The Calm Before The Volatility Storm

The Fed Is Losing Control Of Rates…Stocks Still Don’t Care

US Bond Bear Markets Always End With Turmoil In Stocks

The AI Melt-Up Is Finally Running Into Rates

Nobody Owns Software Anymore… Right As IGV Nears Breakout

The China AI Options Anomaly

Spot Up Vol Up Korea Goes Full Panic

The Quant Trade That Became Everyone’s Problem

Numbers Do Not Matter In Space

Markets Still Refuse To Believe In King Dollar

Schizophrenic Markets

Upside Panic, Nobody Wants Protection

Lot Of MOVEs

The Bond Market Is Starting To Break The AI Melt-Up

King Of AI Cracks

DeepSeek Blues: Deja Vu?

Jamie Dimon’s Favorite FX Brain Is Buying Dollars Again

Tokenmaxxing: Bye Bye Fixed Costs: AI Becoming A Metered Utility Headache

The Bond Market Is Becoming Stocks’ Biggest Problem Again

The Bond Market Is Becoming Stocks’ Biggest Problem Again

We Were Ready To Increase Our Short - Then These Charts Showed Up

Crowded, Leveraged, Fragile

The Most Crowded Trade On Earth Is Cracking

Semis Finally Blink

Gold Is Quietly Becoming The Most Ignored Trade Again

The Europe Comeback Trade Is Quietly Falling Apart

“Different This Time”

Dead Continent Walking? 12 Charts That Scream “Avoid Europe”

Everyone Is Long. Everyone Is Levered. Everyone Thinks They’re Hedged

Tech Has A Rates Problem Again

Everyone Hates Banks

The Momentum Bubble Is Starting To Crack

The Macro Charts That Make Us Nervous

One Of Tech’s Biggest Rotations Is Brewing

Downside Fragility Just Exploded

The First Real Crack In The AI Melt-Up

The Bond Market Just Flashed A Major Warning

Ford Is Apparently An AI Company Now

The Momentum Trade Is One Ceasefire Away From Total Carnage

The Melt-Up Keeps Sucking People In

Downside No Longer Matters

The Most Underpriced Macro Trade?

Spot Up. Vol Up. Breadth Breaking

This Is England: Stagflation, Gilt Stress, And A Slow-Motion Sovereign Decay

Retail Frenzy 2.0: $12 Trillion Army Returns To The Casino

NVDA: Funding The AI Melt-Up

Upside Max Pain

China’s Forgotten Tech Trade Is Exploding

Signs Of Upside Exhaustion

The Bond Market Is Starting To Crack

The Unbuyables: Not Listed. Not Liquid. Not Yours

The AI Melt-Up Finally Started Cracking

Everybody Got Sucked Into The Upside

Rates Are Starting To Matter Again

Nobody Cares About Downside Anymore

Korea’s Upside Panic Just Turned Dangerous

"Madoff Chart" Earnings Keep Going Vertical—What Could Possibly Go Wrong?

The Bro Trade Is Back: Micron, Momentum, And Maximum Degeneracy

Max Pain Market

Silver Leaving Even SOX Behind

Forced To Chase

Nobody Owns Enough China Tech

This Is Not The Time For Zero Hedges in AI

Rally Reservations: Positioning Signals Diverge

The Glory of Low Expectations

The Beautiful Game

Fab Five Fundamentals

Hyperscaler Capex +91% vs Buybacks -64%

Canada’s Housing Bubble Pops… And The “5-Year Time Bomb” Is Just Ticking

Software Squeeze Potential: Positioning Still -4 Sigma

If You See A Bubble, Ride It

Spot Up. Vol Up. Upside Panic.

Europe Is Trading Yesterday’s Economy

Nobody Cares About Silver… Yet

The Return Of Irrational Exuberance

First Crack in the AI Bull

Nobody Owned Enough Upside

6 Of The World’s Top 7 Markets Are In Asia

Software Shorts Starting To Feel Real Pain

KOSPI FOMO Is Getting Dangerous

The Gold Squeeze Setup Is Rebuilding

AI At Discount

“If something can't go on forever, it won't”

Dot.Com Energy Is Back

The Most Hated Tech Trade Is Waking Up

The Entire Market Is Chasing The Same Trade

Silver’s Squeeze Setup Is Back

The AI Melt-Up Just Went Full Panic

Everything Is Squeezing… Not Everything Is Confirming

NVDA: Funding Trade… Or Warning Sign?

Anthropocalypse Now: $1.2 Trillion AI Dreams And Still “Not Enough” GPUs

Oil Is Going Nowhere… But Risk Isn’t

The Upside Pain

Hated Software Starts To Squeeze — And Nobody Owns It

Double Digit Earnings Growth Is Now the New Median

"This Time It's Different"

This Is What Late-Stage Looks Like

This Is What Crowded Looks Like — Now Comes The Test

Rates Are Breaking Things — Equities Just Don’t See It Yet

European Vol Is Screaming. Markets Aren’t — Yet

The Last Leg Of The KOSPI Mania Is Missing

Bitcoin: You Don’t Get Squeezes In Crowded Trades. This Isn’t One.

Seven Charts We Are Watching On Valuations

European Goldilocks gets stuck in Hormuz

No, We Are Still Not There Yet

Not As Good As It Looks Under The Surface

Five Charts That Scream "We Are Not There Yet"

Complacency Meets A Shooting Star

Silver On The Verge… One Push Away From A Squeeze

The Oil Buffer Is The Trade… And It’s Being Eroded

Complacency Is Back… Right On Cue

The Bull Case For A China Macro Comeback Is Getting Harder To Ignore

GS: Bitcoin Shorts At Risk Of Forced Liquidations

China Tech Wakes Up As High-Beta Leads… Laggards Next?

Squeeze Rages As Dip Buyers Get Left Behind

Silver Compressed, Mispriced… Waiting For A Trigger

When Rates Vol Moves… Everything Moves

Goldman credit strategist: "Less concerning than the BDC equity prices would suggest"

The Amount Of Money This Will Cost The US...

Late Length, Short Convexity… Oil Squeezing Into It

The Market Is Still Short Barrels

Gold Isn’t Acting Like Gold

KOSPI Is Ripping… And Ignoring Everything

The Most Crowded Trades In Equities Right Now

The Market Has Become One Trade

Semis Crack… Oil Still Squeezing

XLE Bounced… Now What?

The Semis Move Just Blinked

The 30-Year Is Creeping Toward 5% Again

The 30-Year Is Creeping Toward 5% Again

Oil Is Rising Quietly… Too Quietly

AI Agents Trigger Europe’s €2 Trillion Power Grab

Quiet Index… Loud Risk Beneath

Why Mess With A Good Thing?

The Rally That Won’t Let You In

AI Needs Silver… Silver Isn’t Moving (Yet)

Semis Went Parabolic… Now What?

Dollar Breaks The Model

Nothing Breaks… But Nothing Works Either

The Bid That Never Blinks Is Back Here At ATHs

Looks Like A Breakout… Trades Like A Squeeze

The AI Boom’s First Real Risk: A Political Shutdown Of Its Power Supply

Largest Hedge Fund Selling In 7 Months

"There is no training that can prepare for trading the last third of a move" (Paul Tudor Jones)

Squeeze, Stretch… And Subtle Cracks

Upside Panic Takes Over Semis

The Oil Market Is Still Short Barrels

When Beta Takes Over… It’s Late

Crowded, Extended… And Running Out Of Fuel

Europe Loves Trump: The Accidental Catalyst Behind The 50% Melt-Up

Gold Is Going Nowhere… That’s Still The Trade

The Semis Squeeze Is Going Parabolic… And Getting Dangerous

Is The Energy Catch-Up Trade Finally Starting?

From Forced Buying To Air Pockets Lower

A Fragmented Rally

Stocks Keep Rallying… Everything Else Disagrees

Peak War Trade? Europe’s Defense Stocks Slip Despite Exploding Budgets

China Tech Left Behind… But For How Long?

Bitcoin Is Breaking… And Nobody Cares (Yet)

Post-Software Squeeze

Don’t Buy The Earnings Hype

U.S. Inventory Cycle Shows Signs of Turning

Less Conviction… More Risk

Crowded Upside… Empty Downside

From Squeeze To Chase… And It’s Getting Fragile

The Strongest Bull Market Nobody Owns

BTC “Brewing”: The Most Hated Breakout Setup Is Back

More, More, More: The Corporate Bid Set To Explode

Tesla: Retail Won’t Stop Buying As Fundamentals Keep Sliding

BlackRock: “We view AI as a supercharged mega force"

The Rally Is Starting To Feed On Itself

Break This Level And The Software Squeeze Accelerates

Break This Level And The Software Squeeze Accelerates

The Options Tail Is Wagging The Dog

This Is What Late-Stage Squeezes Look Like

Can Stocks Keep Ignoring Oil?

Someone bought 85,000 SPX 90:1 payout “digi” calls on Friday

China Gains Quiet Leverage Ahead of Xi–Trump Talks

ECB Is Still Fighting 2022

A Different Cycle in Europe: Earnings Hold, Investors Hesitate

Taiwan Bigger Than China

2025 In Disguise? The Same Setup, The Same Squeeze

Inverse Fear Is Taking Over The Market

China’s Fast Money Is Back

Silver Is Waking Up… And Nobody Is Positioned

The MAG Trade Has Turned One-Sided

Sell Low, Buy High: Welcome to the Max Pain Trade

Tech Bubbles And The Roman Empire

Flows Are In Control… But The Setup Is Getting Fragile

Nothing Matters… Until It Suddenly Does

$150BN Of Buying In Days… And It’s Not Over

From Squeeze To Chase: MAGs Go Too Far, Too Fast

From Panic To Calm: Bond Vol Roundtrip

They Shorted Software… Now They’re Getting Squeezed

Morgan Stanley Derivs Desk: Europe Is Capped, Buy America

Morgan Stanley Derivs Desk: Europe Is Capped, Buy America

99.7% Melt-Up Meets 12-Stock Breadth Collapse: What Could Go Wrong?

From Forced Buying To Full-Blown Chase

A Wall of Capital Waits on the Sidelines

Brazil Is Starting to Overshoot

The Energy Flush

The Squeeze Paid. The Chase Will Hurt.

AI Jesus Is Still at the Wheel

Inverse Panic: From Forced Selling To Forced Buying

Silver: Break $80… And This Can Squeeze Hard

Tech Broke Your Brain… Now It Wants $10 Trillion To Fix It

Panic Gone… Complacency Back

IGV: Fifth Test… And This One Matters

IGV: Fifth Test… And This One Matters

BTC: Break $75K… And It Goes

From De-Risk To Re-Risk

The Pain Trade Is Higher Again

The Oil Signal Is Fading

Vol Has Reset… But The Macro Hasn’t

12 Charts That Should Make You Pause

Only 4% Winners: Software’s Brutal Reality Check

Banks Into Earnings: An Update on Flow, Positioning, What's Crowded And How High the Bar Really Is

A Divided Picture Emerges for Europe

War, What War? Stocks Rip As Hedge Funds Chase

The Squeeze Worked… The Chase Is The Risk

Europe’s Bounce Looks A Bit Too Perfect

Vol Reset…Risk Didn’t

They Sold The Lows… Now They Fuel The Upside

From Supply To Squeeze… MAG Is Back In Play

Crash Erased… Squeeze Done

Messy Energy… Now What?

Gold Isn’t A Hedge Anymore

The Most Crowded Trade Just Cracked

This Isn’t About Yields… It’s About Volatility

AI Mania Rolls On: No GPUs, New Highs, And A 400% NVDA Upside Call

From an Earnings Standpoint, the World Is Wonderful

Back To The Middle… And The Edge Is Gone

Brazil: The Trade Everyone Ignored Is Now Printing… Fast

This Is Where Traders Get Destroyed

Nobody Is In… And Silver Just Broke

From Washed-Out To Melt-Up: Korea Rips

Retail Finally Panicked… Right At The Lows

From Breakdown To Squeeze: Tech Just Flipped The Script

Smaller Selloff, Same Setup: Why Gamma Matters Now

The Gold Setup: Long-Term Tailwinds, Short-Term Trap

Downside Needs A Shock… Upside Needs Nothing

What If There Is A Ceasefire?

RIP Traditional Tech: The Bubble Has Burst

Squeeze Or Fade

At The Inflection Point — Now What?

Bond Vol Just Collapsed — Now Watch The Squeeze?

Markets Don’t Wait: Why The Bottom Comes When Everything Still Looks Terrible

Emerging Markets Move in Lockstep With Developed Peers Amid Global Shock

US Tech Is Now Cheaper Than Europe — Here Is Why

Not Running Out of Oil… Just Running Out of Access

Drawdowns Remain Surprisingly Small vs Historical Stagflation Shocks

"Sell Everything Europe": 3rd Biggest Dump In A Decade As Flows Go Full Capitulation

Selling Extreme, Conviction Missing

Silver Stuck In Chop As Pressure Builds

Silver Stuck In Chop As Pressure Builds

The Bounce Just Failed — Now What?

Extreme Oil, Extreme Vol… What Breaks First?

Goldman: "Don’t wait for the conflict to end to buy Agentic AI"

Violent Bounce Hits Resistance: Trap Or Turn?

From Overbought To Support In 3 Days — XLE Just Reset

The Easy Part Of The Bounce Is Over — Now Comes The Hard Part

SPX Can Handle Rates — It Can’t Handle Bond Vol

Brazil Is Quietly Becoming The Cleanest EM Trade

The Great Mag 7 Unwind Is Done — And Nobody Is Positioned For The Upside

The Economic Impact of Higher Oil May Be Smaller Than Feared

They Sold Everything… Then Got Squeezed

Silver Squeeze Setup: The Turn Is Starting

Gold Stabilizing After The Puke — Squeeze Setup Brewing

They Chased Korea… Now They’re Trapped

CTAs Puked. Dealers Short Gamma. Squeeze Setup Is Here

To capitulate, or to have capitulated, that is the question

The Crypto Ecosystem In Survival Mode: Volumes Collapse, Funding Dries Up

Everyone Is Looking For The Bounce — And That’s The Problem

The AI Trade Everyone Loved Is Now Breaking Down

The Most Perfect Trade In The Market Is Getting Dangerous

Oil vs Inflation: One Of Them Is About To Be Very Wrong

Earnings Hold Up, Even as Markets Waver

China Loves the Iran War

If You Believe in Voodoo and Small Quant Studies

So Close to a Magnificent Bear

European High Yield CDS At The Widest Level Since April

This Is The 3rd Largest Hedge Fund Selling In Over 10 Years

The Déjà Vu Breakdown

Markets Are Finally Pricing Fear… But The Fast Money Has Already Sold

From Flow Shock To Depletion, Oil Enters Its Next Phase

MAGs Are Bleeding Out—And Now It’s Accelerating

Markets Are One Break Away From Getting Ugly

EM Is Cracking Just As The Crowd Piled In

Software On The Brink: Break…Or Violent Squeeze

Looks Orderly… Until It Isn’t

One More Oil Squeeze… And Something Breaks

100 Days Since the Tech Peak

The Bounce… Or The Breakdown?

Equities Look Calm… Everything Else Disagrees

Bond Vol Screams Stress… Equities Aren’t Listening

The Gold Vol Flip: Panic Hedging Sets Up A Squeeze

EM Is Breaking… Brazil Isn’t

Hit it when it is down: 11 more charts of why Europe stinks

Good Enough For a Short-Term Bounce?

Chaos Markets: Pressure Is Building Everywhere

XLE Won’t Stop…Until It Does

EM On The Brink: Rates, Oil, And Vol Collide At A Must-Hold Level

The 4.4% Line: If The 10-Year Breaks, Everything Changes

Gold Prints A Hammer As "Smart Money" Buys Puts

Financials have the biggest underweight across sectors

Back Inside…But Nothing Feels Stable

Massive Oil Move…But Uncertainty Isn’t Going Away

Software: The Squeeze Setup Builds

Buy High, Sell Low: The Max Pain Market Lives On

Silver Hits Range Lows As Hammer Traps Late Sellers

From Safe Haven To Pain Trade: Gold’s $1000 Collapse

Yet Another "Annus Horribilis" For Europe

Seven Things That Have Yet To Break

That Was Quick! Tech Now the Most Discounted Sector in the S&P500

The Rates Market Is Losing Control

Hello Stagflation, My Old Friend

Are We There Yet?

From Grind To Crack

Ripping Rates, Rising Vol, Rising Risk

Silver’s Most Dangerous Phase: The Chop That Destroys Both Sides

5-Sigma Selling, Short Gamma And Oil Stress. What Could Go Wrong?

Make-Or-Break: Markets Hit The Edge As Oil Decides Everything

The NASDAQ vs S&P500 Implied Vol Spread Is Approaching Multi-Year Lows

DAX At The Edge — Europe’s Make-Or-Break Moment

From Darling To Disaster: Gold’s Crowded Trade Starts To Unwind

From Grind To Break? The Most Dangerous Market Is The One That Won’t Panic

European Pharma Not Acting Like a Safe Haven

Cracks Forming As Markets Press Key Support

Silver’s Hangover Isn’t Over — The Unwind Continues

Gold Is Not A Hedge — It’s A Crowded Trade

Europe Is Getting Hit From All Sides — And The Euro Is Cracking

KOSPI Surges 5% As “Upside Panic” Returns — And It’s Not Even Overbought

Bernstein says NVDA "almost absurdly valued"

The Most Frustrating Market In Years

Ten Charts That Caught Our Eye

Credit is getting attractive

Rates Trapped — Oil Dictates The Next Move

The Grind That Breaks Hedges: Why Markets Refuse To Crash

EM blues: 2022 déjà vu as oil risk and USD strength collide

The Strongest Tightening Shock Since 2023

Oil Is Driving Everything

The Oil Trade Everyone Owns — And That’s The Problem

After “Banks Breaking Bad,” Is This Just A Dead-Cat Bounce?

Oil’s Panic Rally Shows Signs Of Exhaustion

Gold Breaks $5K As The “Safe Haven” Narrative Cracks

"Europe to be hit by an inflation tsunami"

8 Charts Challenging the ‘Buy the Dip’ Narrative

EM On The Edge: Record Buying Meets Rising Oil And Exploding Vol

“As The Banks Go…” – And Right Now They’re Breaking Bad

SPX Stuck In Range As The Big Short Builds

Dollar Breakout, Euro Breakdown

Korea Abandons KOSPI… Starts Chasing Bitcoin Again

Retail Is Piling Into Energy At The Top

Rates Volatility Erupts, And Stocks Should Be Nervous

VIX tends to peak and SPY trough in mid March

Searching for signs of capitulation

Oil Chaos, Déjà Vu Signals, And Gold’s Hedge Problem

Gold Isn’t Acting Like A Hedge

Déjà Vu: The Setup That Triggered Last Year’s Selloff Is Back

When Oil Trades Like A Meme Stock, Something Isn’t Right

Oil Volatility Is Exploding — And Something Is Starting To Break

Putin’s Ghost Haunts Europe Again—But The Setup Isn’t 2022

Oil “VIX” At 121 — Markets Aren’t Pricing De-Escalation

Oil Chaos Is Crushing Europe

Silver’s Bubble Is Still Deflating

Oil Volatility Is Running The Market

Everyone Long Energy — Now What?

VLCC rates above COVID highs. Jet fuels hit record highs

It ain't over till the fat derivatives lady sings

Oil Volatility, Short Gamma, And A Fragile Market

Korea Trades Like a MEME Stock — and an Oil Vol Proxy

The Calm Market Illusion

Still Stuck — But The Market Just Became Very Fragile

Crude: The New Meme Stock?

More Charts From The Software Panic & Bounce

Everybody Wrong

Hammer In Stocks, Shooting Star In Oil

Software Is Extremely Cheap — Another Squeeze Coming?

Extreme Fear Returns — Stocks Still Clinging To The Range

MOVE Is Back: Stocks Should Pay Attention

Mission Accomplished: Oil Just Printed A “Shooting Star On Steroids”

From War To Wheat: Hormuz Disruption Ignites Food Inflation Fears

Europe is back! (Flirting with recession)

Monday Mayhem Setup: MoMo Crash, CTA Sell Signals And Retail Still “Buying The Dip”

Oil Shock: 17x Larger Than The Russia Supply Hit

How Much Selling Did We Actually See Last Week?

What A Week!

Oil Volatility Hits 103 — Global Panic Builds

Oil Panic: Volatility Explodes As RSI Hits Kuwait War Levels

Oil Shock Meets Bond Volatility — And 4.2% Is The Line In The Sand

Silver’s Speculative Blow-Off Is Still Unwinding

Gold Is Stuck — Oil Panic Is The Real Crisis Trade

"The inflection supports our call for decade-high US Industrial growth into 2H'26 & 2027"

Missiles In The Headlines, Brunch In The Malls

Exploding Oil, RoW Panic, And A Violent Software Squeeze

Software Shorts Carried Out On Stretchers

Korea K-rashing As EM Volatility Explodes

Europe Breaking Bad As Volatility Explodes

Everyone Loves EM — Just As Volatility Explodes

Oil Breakout Meets Extreme Geopolitical Risk

The Attack On Europe

Hyperscaler capex already accounts for ~10% of US gross capital formation

Stocks Still Stuck — Oil Volatility Remains Elevated

Bond Volatility Just Woke Up — Stocks Usually Don't Like It

Wall Street Is Massively Long Semis — And Massively Short Software

Signaling an “Attractive” Set-Up

Bitcoin Is Quietly Brewing

Parabolic Moves Never End Well — The KOSPI Bubble Just Found Out

The Grand Old Man Of Strategy Warns: "Near-Term Risks Are More Elevated"

The Grand Old Man Of Strategy Warns: "Near-Term Risks Are More Elevated"

The Surface Is Calm. The Structure Is Not.

Korea’s Leverage Trade Just Blew Up

Volatility Shock: Panic Is Spreading

Oil Volatility Explodes As Markets Brace For A Bigger Shock

Did Gold Just Print a Blow-Off Top?

The European Unwind Has Begun

KOSPI’s Parabolic Bubble Meets Forced Liquidation

Largest Amount of Put Protection Ever

Oil Overbought, Hedging Extreme, Dollar Testing Breakout

Downside Desperados: Panic Bid For Crash Protection

Silver Mania Just Found Sellers

The Dollar Everyone Hates Is About To Squeeze

Either Commodities Are Wrong — Or Inflation Is About To Matter Again

Oil: $75 Is Noise. $100 Changes Everything

Oil: $75 Is Noise. $100 Changes Everything

Big Tech´s Largest Underperformance Since Mid-2024

Everyone’s In, No One’s Sure

Cyclicals vs Defensives Had the Worst Week of the Year

Are We Still In the Early Innings of a Massive Emerging Market Rotation?

The 15 Charts That Should Make You Uneasy

EWY Weekly RSI 90 — Parabola Territory

Is Something Cracking Beneath The Surface?

The Energy Squeeze Isn’t Done Yet — Oil Is Setting Up

The Most Crowded Trade In Tech Is Starting To Unwind

Credit Rarely Moves First Without a Reason

Made in Korea: Volume, Vol and Leverage At Extremes

The Curious Case of Cheering for German Military Spend

The Squeeze Is Rotating

Nothing NVDA — But Something’s Shifting Beneath The Surface

Silver: Miners At ATHs, Skew Exploding — Breakout Or Violent Unwind?

Record Underweight, Massive Short, Historic Oversold — Software’s Explosive Setup

Private Capital’s New Liquidity Cycle

The FOMO Class Now Boarding the Seoul Train

When Everyone Buys Puts…

RSI 89. Vol Spiking. And Still Cheap?

Massive Weekly Hammers: Crypto Defends the Line in the Sand

Inflation Is "Gone"… Until You Look At Commodities

Fed Enters AI Panic As Tech Sits On Massive Support

A Turning Point Approaches for Big Tech Spending

AI Fear Peaks, Software At GFC Extremes — Right Tail On Sale

The Rise of the Robots

The AI Trade Didn’t Die, It Moved To Korea

Apple Becomes The AI Hedge — And The Squeeze Is Building

The Software Breakdown: Massive Volume, Extreme RSI, Panic Term Structure

Silver’s Broken Vol Market Meets Structural Demand Risk

Crowded Semis, Gamma Gone, Squeezy Gold

Remember What Markets Did Last Year? It’s Setting Up Again.

Gold Breakout Or Blow-Off? Monthly RSI 96 As Dealers Fuel The Rally.

XLE Shorts Carried Out On Stretchers As Oil Breaks Trendline

Semis: The Most Crowded Trade On The Street

Heavy De-Risking In A Stuck Market — Is The Pain Trade Higher?

Everyone Is Hedged. That’s The Problem.

Underestimate This Economy At Your Own Peril

More extended hedge fund positioning meets Trump's new tariffs

Moribund & Maligned or Maturing & Mispriced?

Will We See The Normal "Stock Down Vol Crushed" Post NVDA Earnings?

Extreme Shorts

Second Largest Sale Ever

Over-Hedged Markets, The Capex Paradox, And A Brazil Squeeze

Nobody Owns The Right Tail

Bull Do Brasil — Druckenmiller Is Already In. Are You?

The Capex Paradox: Who Funds AI If AI Stops Paying?

Roaring Russell, Richer Skew And Diverging Vol — Something Is Brewing Under The Hood

Goldman’s Dominic Wilson Says the Cycle Still Has Room to Run

Goldman on Gold: The Risk of a Margin-Related Liquidation Sell-Off

The Best Offense Is a Good Defense

Fragile Tech, Vertical Korea, And Exotic Carry

A Little Lower… And It Gets A Lot Worse

Software At The Edge: $80 Or Air Pocket

No Substitute: Uranium At The Center Of The AI Power Shock

3 Oil Charts We Are Watching

KOSPI Beast Mode: Another +3%

Fancy Frontier FX?

Global Yields At Critical Inflection Levels

Rare Internals, Crowded Dollar Shorts And A Brewing Oil Squeeze

Everyone Is Betting Against King Dollar

The Oil Squeeze Setup Is Building

The Market Looks Calm — That’s The Trap

A Bullish Letter from Corporate America

The Startups That Wish for War

Cash Burn, Tech Stress — And $134BN Of Selling Risk

Apple — Is The Anti-AI Trade Starting To Work?

The Market Has A Downside Convexity Problem

The AI Trade Is Being Questioned

Under-The-Hood Panic Is Building — And Spreading

Are You Software in Disguise?

Silver Mania Is Over — And The Late Bulls Are Trapped

Life After Goldmageddon – Boring Is The New Up

The Dangerous AI Trade

Europe Continues To Trade With A Steadier Rhythm

Global Growth is About to Pick Up Big Time

This Earnings Trend Is A Bulls' Best Friend

Systematic Tsunami: BofA says there could be $130bn of selling this week

MEME 2.0: Traders at the Casino

SaaS At Zero Percentile

Eating All The Cash: Hyperscalers Spending 92% of Cash Flow on Capex

NASDAQ On Edge, CTAs Lurking Below — And Fear Still Elevated

Fear Running High Into The Long Weekend

Bounce Or Breakdown?

SPX Hates Rising Bond Vol — And MOVE Just Woke Up

AI Panic Crushes Software — But Is The Market Dead Wrong?

"We haven't seen anything like this since the dotcom bubble burst..."

When the (AI)iens invade

Same Setup As Last Year — And It Didn’t End Well

Stressed Silver Slips

Remember Fear?

The Mag 7 Setup: Chop Now, Violence Later

While You Watched NVDA, Korea Built A Monster Bull

$666bn For GPUs, $250bn For Cures: Welcome To Peak AI Insanity

King XLE: Squeeze, Surge, and a Full-Blown Re-Rating

Flat Index, Violent Rotation, Stressed Tech

The Calm Is a Lie. Tech Stress Refuses to Mean-Revert

Oil Calls Aggressively Bid — Squeeze Loading?

Gold Just Flushed $13.7BN — And It’s Still Standing

JPY Carry Time Bomb: VIX About To Detonate?

CBO Says Immigration To Return Back Up To Historic Levels

25% Growth (!) EM Just Got Even Louder

Surging Skew, Stabilising Software, Stalling Silver

Software Puked. Shorts Are Crowded. Bounce Is On

Life After Silvergeddon: Bagholders, Broken Vol and a Fading Bounce

Tether Is Quietly Becoming a Gold Whale

11 Charts Why EM Is Crushing It

3 Gold Charts We Are Watching

Risk Is Packed, Credit Is Crowded, Protection Is Thin

Software Capitulation Meets a Violent Rotation

Vol Is Calm on the Surface — Tech Stress Isn’t, and Skew Knows It

Everybody Hates Software — And That’s the Setup

Three Charts to Watch: What If MOVE Starts to Move?

When AI Runs Hot in Asia, BTC Loses Its Bid

King Russell, Broken Tech and Violence Beneath the Tape

From Tokyo With Love: Yields Threaten Another Squeeze — Gold Is Watching

ATH While Everything Else Wobbles: Pharma Is The New Safe Haven

Doubling Up On Europe: From "Less Bad" to Actually Interesting

Is Tech Screamingly Cheap Now?

Tactical Upswing Confirmed

The IPO Window Is Reopening. And This Time It’s AI, Musk, and a Trillion-Dollar Question

Bubble Behind: US Tech Stocks Now Trading at 5-Year Valuation Lows

A Flush Without a Cleanout

King SOX Flexes. Software Hits Do-Or-Die. Gold Cleans Out Excess.

Do Or Die For Software

Gold Cleans Out The Excess Without Killing The Trend

Déjà Vu Is Getting Dangerous — NASDAQ Replays The 2025 Breakdown

Stress in Software Begins to Surface in Credit

Crowded Semis, Software Smoked, Silver Slaughtered

Bitcoin Gets Massacred: Narrative Dead, Structure Broken

Checking In On The War Defense Trade — And The Squeeze Is Gone

Goldman Compares Software to Newspaper Stocks

Post-Silvergeddon: Bagholders, Broken Vol, And Bidless

Carnage — The Momentum Puke Is Bigger Than DeepSeek

Say Hello To $70k — Bitcoin’s Software Meltdown Is Accelerating

Europe Begins to Find Its Footing, Perhaps...

Thinking About Bottom Fishing in Software

Tech Stress Explodes

Tech Cracks, Stress Explodes — But Software May Be Hitting Exhaustion

Software Smoked — RSI at 16.9

Precious Metals: What Comes After the Bounce?

Software Panic Hits 2011 Extremes — Mean Reversion Signals Are Triggering

A Few Old Gold Bulls Crawl Back Out of the Bunker

Software Exodus & Small Cap Tech Flush

Battered BTC — From Obsession to Apathy

Software Cracks, Credit Blinks — SPX Still Pretends as Downside Convexity Builds

Gold and Silver Bounce — Dead Cat or Reload?

Asia Is the AI Sweet Spot — NVDA Is Yesterday’s Trade

Tech Is Still Up—But the Internals Are Breaking

10 Reasons Why We Are Bullish Europe

Precious Indecision, Dollar Power and Seriously Long Systematics

The Boring Bull Case No One Wants to Hear

The Dollar Comeback

From Parabolic To Panic: Korea’s Trading Frenzy Breaks

Trump-Coin: Backed by Approval Ratings, Volatility, and Vibes

Silver After The Crash: No Control, No Conviction

Gold Approaches First Key Support — Will It Hold?

Something Bad Is Lurking Under the Surface

From Melt-Up To Margin Call: Precious Metals Repriced

The Protein Trade: From Bodybuilders to GLP-1s to Wall Street

AI Capex Was Supposed to Peak. It Didn’t.

Everyone Is Long the Same Thing Again

Warshed Out — When Parabolas Break, Nothing Else Stays Standing

No Shorts, No Cash, No Protection

Soggy BTC: $80K Is Make-Or-Break

Silvergeddon Unleashed

Gold’s Resonance Just Broke — Vol Screams As Late Longs Pile In

Microsoft and Software Get “Epsteined” And Leaving a Trail of Suicide Notes

Black Gold, Lazy Longs And Shanghai Hoards

Supply Rises Fast Below The Tape

Oil Blows Through The 200-Day As Upside Panic Kicks In

Everything Goes — Again

Goldmaggedon: From Shanghai With Love

The Return of the King of Detroit

SPX Stuck While The Rest Of The World Melts Up

Is This Really A Dollar Breakdown?

Range-Bound Stocks, Restless Vol

The (Very Old) Empires Strike Back

Asian AI Bullies Bitcoin And Leaves NVDA Behind

EM On Fire: Upside Panic Takes Over

Why There Is Still Juice in the Tax Trade

Brazil Bonanza

Dollar Breaks, Gold Gets Crowded and Asia Runs AI

Watching Gold Volatility Is Key From Here

JPY Rate Check, No Checkmate — No Vol Panic

It Will Take Years for Housing Affordability to Normalize

Asia Is AI

How to get to 6666 in Gold

"The Need to Future-Proof": Goldman Partner on the Current M&A Boom

JPY Risks, VIX Shorts & Silvergeddon

Silvergeddon

Gold Vol Finally Panics — What’s Next?

Doomed Dollar’s Delicate Moment

JPY Risks You Must Watch

Europe Wants AI. It Can’t Plug It In.

Europe’s Achilles Heel: Too Much Momentum

Déjà Vu Is Back: Fading Momentum, Massive Systematic Longs, Serious Downside Convexity

EU Luxury: A Tactical Bottom or Continued Hangover?

Short Vol, Long Leverage, Buy the Dip — A Recipe for Disaster

Meltdown Melancholy & Mad Volatility

Hard Assets Hot, Yen Breaks, Rates Still Asleep

Russell Takes a Much-Needed Pause — But The Bull Isn’t Done

3 JPY Charts To Watch

What If That Second Wave of Inflation Is Upon Us?

Bull Do Brasil

Something Is Wrong in Rates

Big in BCOM — This Is What a Real Breakout Looks Like

Incredible MOVE — Why Falling Bond Volatility Matters

Russell Breaks Out as AI Heats Asia and Gold Panics

Gold Vol Panic Builds as Retail and CTAs Pile In

From Squeeze to Slam — Defense Momentum Breaks

Russell — Overbought, Overlooked, Overperforming

Asia’s AI Engine Is Red-Hot While the West Chases NVDA

Do Bad Charts Fix Good Stocks?

Growth Is Back. So Is Potentially the Inflation Problem

Golden Reversal Meets Golden Upgrade

SPX Stuck — Silver Soft, Gold Stretched

Golden Reversal — Blow-Off Starts?

Bitcoin’s Myths Are Breaking — Hedge, Store of Value, Now Quantum Risk

The Mag 7 — Heavy, Tired, and Still Soggy

Silver Looks Untouchable — But Indecision Is Creeping In

Déjà Vu? — This Is How It Started Last Time

Should You Take a Bite of the Rotten Apple?

VIXplosion — What Now?

Everything Goes — Cross-Asset Selling Hits Fast

Bond Vol Goes Brutal — Biggest Shock Since “Liberation Day”

Gold Thrives as Japan’s Bonds Break — Geopolitics Add Fuel

VIX Goes Violent — Investors Still Treat Protection Like It’s for “Suckers”

30Y JGBs in Full Panic Mode — Global Spillovers Have Started

Highest Expectations in 15 Years

Surging Silver — AI Eats the Moat, Credit Picks Up the Tab

Super Silver Is Exploding — Don’t Look Away

Roaring Russell — Too Much, Too Fast?

Upside Rates Panic — Japan’s 10Y Is Unhinged

Everyone’s Long. Charts Are Rolling. Vol Is Waking Up.

Tariff Talk Is Loud. Europe’s Turnaround Is Louder.

Meta-verse became Meta-wide

AI Ate the SaaS Moat

Femcels & Fentanyl

That Was the Soft Launch - Now AI Is Leaving the Screen

The Risk-On Reflation Trade Is Back

Calm Is Crowded — Contrarian Sell Flashes Red

Vol Is Dead — And That’s the Opportunity

Silver 100%+ Above the 200-Day — Vol Sets the Trap

MAG 7 Is Tired: Only One King Left Standing

They Seek It Here, They Seek It There...

If You See A Bubble - Ride It

SPX Is Trapped — Bulls Take Over, Bears Gone

Small-Cap FOMO Is Exploding — Russell Breaks Out, Crowd Wakes Up

Could Rates Rise From Here?

Silver Has Entered the Danger Zone — Volume Explosion

Amazon Trades at a Discount to Walmart — Let That Sink In

3 Bond Vol Charts We Are Watching

Small Caps Take Control as Big Tech Wobbles — Vol Warns, Silver Goes Wild

Range Highs Bite Back — NDX Triple Top as VVIX and Skew Whisper Trouble

Silver Has Left the Building — Vol Is Broken, Ratios Are Crashing, Bubble Alarms Are Screaming

Gold Keeps Ripping — But Bubble Signals and the Dollar Gap Are Flashing Red

Chasing Oil, Silver, Dollars, US Futures and VIX

The Calm Is Lying

Dollar Charts That Matter Right Now

Oil Is Breaking Out — And The Crowd Isn’t In

From Japan With Chaos — The Yield Shock No One Wants

VIX Shorts Are One Shock Away From Forced Buying

Will India Get Revenge?

400 Professionals. One View. What Could Possibly Go Wrong?

China Tech Squeeze Is On, Metals Go Full Upside Panic

Luxury: Under-Owned, Under-Loved, Turning

The Super Silver Squeeze — Extreme Momentum, Crowds Still Missing It

Gold Won’t Stop: New ATHs, RSI Extreme, Still Under-Owned

China Is Squeezing: 17 Up Candles, Tech Ignites

"Do you really want to pick a fight with this trendline?"

How Stretched Is Positioning?

Europe's Bull Case Is Still: "It Can Only Get Less Worse"

The Good, The Bad and The Ugly on Valuation

The 15 Fundamental Charts That Caught Our Eye

Breakout or Bull Trap? Valuation Hubris Means No Room for Mistakes

Europe's Energy Transition Is Entering a New Phase

King Dollar Breaks the 200-Day While Funds Flip Short — Uh Oh

Oil Just Snapped the Downtrend

The Offense in Defense Is Getting Crowded

Schhh — Shanghai Soaring

Old Grumpy Economists See Recession. Sexy Miss Market Sees Acceleration

Late Cycle, Elevated Valuations — And Goldman Is Still Bullish

The Easy Trades Are Getting Hard

Small Caps Are Breaking Out While Everyone Watches Tech

Everyone Hates The Dollar — That’s The Problem

Tech Goes Nowhere As Stress Quietly Builds

Silver Euphoria Meets Reality

The AI Ate My Buyback

Emerging Markets For Dummies

VIX Is Too Quiet At The Wrong Time

Everything Looks Fine… Right At The Range High

The Panic To Defend

Forced Selling Is Coming For Gold And Silver

Everything Looks Bullish… Right At The Range High

"S&P is higher in nearly 9 out of 10 years when GDP is growing; bull markets usually end with hikes, not cuts."

The Start of Something Huge? Goldman Sees 20% Upside in China

Reflation Signals Are Spreading — Commodities, Silver, China

Silver on Steroids - Can’t Keep a Good Man Down

Remember Oil? The Most Ignored Reflation Trade

No Inflation… Unless You Need Commodities

Bond Vol Is Dead… Long Live Bond Vol

China Is Breaking Out, The Forgotten Market Is Ripping

Positioning Remains Supportive, but of Course No Longer Light

This Bitcoin Chart Is Triggering Squeeze Déjà Vu

Precious, Oil, Crypto, AI, Defense — Everything Is Squeezing

Unstoppable: Japanese Rates Keep Climbing

War Risk Is Back on the Tape — Defense Stocks Explode

Silver: Bubble, Blow-Off, or Something Bigger?

Silver: Bubble, Blow-Off, or Something Bigger?

Gold Is Setting Up Another Leg as Seasonality Turns Sweet

Asia’s AI Risk-On Siren Is Blasting, Again

Five Bullish Signals to Start the Week

Germany Is the Problem

The Greenback’s Problem: What Happens When the Inflows Stop?

Could Drop 99% and Still Beat S&P500

From Mom’s Basement To $6bn In 12 Months

Europe Rallies, Hedge Funds Sell Anyway

When Boardroom Animal Spirits Are Unleashed, They Don’t Stop Quietly

Mag7: One Last Look Before the Year Ends

Silver Goes Full Metal: 1979 Vibes

Gold: $31.5 Trillion, New Highs, And Still “Early”?

The AI Ouroboros: Big Tech Eats Its Own While Capital Loses All Meaning

A 10-Signal Cluster-F*ck

Santa Is Late, Not Dead — And Positioning Says There’s Ammo Left

The Vikings Just Killed Santa

Five Quiet Signals Suggest the Bull Case Isn’t Done Yet

Silver Is Flying, But Options Say Slow Down

The Great Vol Smash

Trust the Perfect Netscape Trajectory Or the Flashing Sell Signals?

Bond Vol Is Screaming ATHs for SPX

Positioning Isn’t a Problem - But Margin Debt Is

Rangebound Markets, Extreme Metals, and Late-Cycle Warning Signs

Gold: Under the Hood, Upside Panic Is Huge

Silver: Record Overbought, Volatility at Extremes

AI: Not a Bubble, But Not a Free Lunch Either

The World’s Hottest Stocks Have Gone Nowhere

From Sexy To Soggy: SOX Is Breaking At The Worst Possible Time

The Latest on Positioning

Japan’s 10Y Is Running the Show And Markets Should Be Nervous

Commodities Back at Support: Second Chance?

Crowded Shorts. Cash Gone. Big Bid About to Fade.

Interest Costs Are Exploding And Yields Are Still Rising

Everyone Owns Semis, Nobody Owns Software: Guess What Happens Next

The AI Trade Is Losing Its Footing as Asia Flashes Red

Everything Ex-Hot Is Getting Sold

Bitcoin’s at the Edge: Who’s Gonna Buy?

Gold Goes Vertical — Again?

The Japan Rate Shock Is Hitting AI

The AI Trade Wobbles: Asia’s Bellwethers Flash Yellow

The Long End Revolts — You Should Be Nervous

AI Was the Trade, Now It’s the Problem

This Is How Rate Accidents Start

Everything Is Bullish Except the Price

Gold Is Loading at ATHs While Volatility Sleeps, This Is How Squeezes Start

Double Top Déjà Vu or the Squeeze of the Year?

Russell Rips, Silver Explodes, AI Wobbles

Silver Shorts Carried Out on Stretchers

AI – Dream or Delusion? The Cracks Are Getting Hard to Ignore

Small Caps Go Beast Mode

Russell Roars, SPX Squeezes - and With No Bubble…

Cold Crypto Breeze - No Buyers, No Flows

This is The Cheapest Hedge in AI/Global Macro

VIX Sleeps, MOVE Moves - Who Do You Trust Into FOMC?

SPX Stuck, Rates Unstuck, Silver Panics

Gold’s Catch-Up Moment? Vol Cheap, Firepower Untapped

Silver on Fire: Vol Bid, Skew Explodes, CTAs Chase

If You Want Peace, Prepare for War: Europe Is Re-Arming

Rates on the MOVE - And the Market Isn’t Buying the Fed

Sell Low, Buy High - And Ignore the Code Red?

From Agony to Euphoria - But First Watch These Charts

3 Bond Charts We Are Watching

AI’s Forgotten King Roars Back

Europe Edges Higher as the ‘Less Bad’ Narrative Holds

Banks, Bankers & Breadth - Breakouts Everywhere — Choose Your Mania

A 3 Sigma Week: When Everyone Hit the Risk Button

Big China Flows Exit… Just as the Charts Start to Turn Up

Altman Goes Full YOLO While China Builds Top-Tier AI for Pennies

Markets Are Heating Up Everywhere - Except in the Trades People Worship (BTC, NVDA)

30Y Breaks Out, TLT Breaks Down - Strap In

Commodities Are on Fire - Breakouts Everywhere, Oil/Energy Up Next?

Gold’s ATH Setup Is Here: Explosive Seasonality Meets Surging JGB Yields

SPY Shorts, Crap Squeezes, and Asia’s Wild Tails

US 10-Year Keeps Trying, Yield Gaps Rip Wider, and Treasury’s Interest Costs Close In

China’s AI Awakening: A Coiled Market Ready to Rip

The Widowmaker Awakens: JGB Panic, Yen Surge, and a Global Deleveraging Trap

America’s New Housing Fix: A Mortgage You Can Die With

Today We Choose Violence: The Anti-Narrative Edition

The Wrap: Rotations Heat Up - and Volatility Sleeps… For Now

The Charts Keeping Us Awake at Night

Vol Panic Dead, Protection Puked - Now VIX Seasonality Sets the Trap

Japan’s Yield Surge Is No Local Story - Remember What Happened to the NDX Last Time?

The Wrap – Divergences Everywhere: Rates, Vol, AI, Crypto, Gold

Bitcoin Bros Are Back?

Gold $5k – Surging Flows and a Market Still Massively Underweight

Remember Rates in October? The Setup Is Back

The Wrap: SPX Stuck, BTC Cracks, Silver Screams, and Japan’s Bondquake Spreads

China Tech Wakes Up

Sexy Silver’s Squeeze 2.0

Bitcoin’s “Everything Hedge” Myth Dies: JGBs Blow Out, Trend Breaks, Death Cross Hits, and MSTR Turns Toxic

Bondquake in Tokyo - Yield Spreads Hit Absurd Extremes, Something Has to Break

10 Things Not to Be Thankful For This Monday Morning

"This may bode well for both upside and market breadth"

Europe Claims It’s “Recovering” — The Charts Say It’s More Like Crawling Out of a Hole

AI Wants Your Job — And Now It Wants Your Electricity Too

The 10 Charts We Are Watching This Saturday

The Wrap: AI Darlings Don’t Buy the Bounce - But Metals Sure Do

Gold Breaks Out. Silver Explodes. Volatility Erupts. Are You Still Flat?

Thanksgiving Coma: Fear and Panic Both Passed Out

If AI Is Really Booming, Why These Divergences?

Fear Implodes - What’s Next When Vol Dies and Bargains Emerge?

Soggy Asian AI - But Is This Re-Load Time?

The Wrap: Big Short Meets Big Buy and a BTC/VIX Plot Twist

It Was Useless as a VIX Hedge - Now Does BTC Rip as Vol Collapses?

Gold Breakout Brewing: Central Banks and Retail Are Loading Up

Healthcare Mania - Hedge Funds All-In, XLV Most Overbought Since 2018

Panic Out, Panic In - Heavy CTA/Short-Gamma Selling Followed by the Largest Two-Day Buy in Months

The Wrap: Keep It Simple - Just Follow the 10-Year

Gold's Consolidation Ending? Skew Suggests Squeeze

Google's GPU Killer - Phase 2

Fed Cuts > AI - The Only Thing That Matters

The Dog That Didn’t Bark: Asia’s AI Sentimentors Stay Dead Cold

The Wrap: Just Buy It – Bottom-Shorting Meets Shitty Liquidity

They Shorted the Lows Again – Max Pain Market

Google – From “Search Is Dead” to “TPU Beats GPU”

BTC Bleeds – Death Cross, Outflows, and Shitty Liquidity Collide

Corporate Animal Spirit Is Back

From Market Darling to Macro Dead-Weight: Germany’s 2025 Dream Unravels Fast

AI Megacaps Throw Off New Warning Lights — Or New Fuel — Depending on Your Religion

We have not seen Goldman this bullish China in a long time

Was That the Last Flush?

Market Flush, Gamma Chaos, NVDA Hammer, Santa Window - This Is the Setup

MAG Charts to Watch - Big Levels, Big Decisions

Systematics on Edge - Short Gamma Pain, but NVDA Still Runs the Market

Asian AI Darlings Crack - KOSPI Volatility Blows Out

Bitcoin: Store of Value? More Like You’re Shorting Volatility Without Knowing It

The Wrap: Semis Break, Skew Screams, and Cash Is Gone

Fear Explodes, Japan Melts Down And Massive Systematic Downside Convexity Looms

China’s AI Edge: Infinite Power, Infinite Upside, Superior ROI

Tokyo Bondquake - Bond Volatility Screams “This Isn’t Contained”

The AI Bubble Exposed

The Dollar Breakout - Bears Trapped as DXY Closes Above the 200-Day

The Wrap: The Big Long, The Big Short, The Big Fear

Bitcoin Bids Wanted

The Surge In Fear

Japan 30Y Breakout Moves Everything - AI, Crypto, Gold, Even NVDA

The Wrap: Volquake: Puts Explode, MOVE Screams, Tech Spreads Snap

Gold’s $4K Line Holds - Again

Fear Is Back - So Is Put Love

Asia’s AI Darling Just Blew a Fuse

The Wrap: Trend Lines Snap, Small Tech Smoked, CTAs Sweat

Bondquake in Japan - VIXquake in the US

Tech Hedges Bought, NVDA Nervous, Downside Convexity Lurking

Healthcare Wakes Up - Biggest Bid in 4 Years

Bitcoin’s Oversold, Hated, and Sitting on Support - Perfect.

Closing the Gap: Europe’s Quiet Return to Competitiveness

AI, GDP, and the Bull That Forgot to Breathe

Fart Coin Better Than Melania Coin

The Wrap: Nobody in Control

Friday Déjà Vu: Short Gamma’s Sell-Low/Buy-High Agony Returns

Gold’s “Fear Hedge” Dies - VIX Explodes, Gold Implodes

First Trend Breakdown Since May: 50-Day Snaps

AI’s Asia Meltdown - KOSPI Cracks, SK Hynix Gets Nuked… and the Spillover Risk Is Massive

The Wrap: The Puke - Small Cap Tech Crashes, Vol Pops, Crypto Cracks, Gamma Bites

Lower Highs, Exploding Bond Vol, Small Cap Tech Bleed… and CTA Downside Convexity Waiting Below

The LATAM Bull - The World’s Most Exciting Market Is Not Where You Think

Silver on Steroids - Upside Panic Is Back

Bond Volatility Soaring - Will It Spill Over to SPX?

Parabolic or not in AI

Keep Calm and Debt On - AI Borrows, Gold Gets Loud

Gold’s Furious Rebound

Europe’s Back - Breakouts Across the Board

Divergences We’re Watching

AI on Steroids - The Bubble That Refuses to Die

The Wrap: To AI, or Not to AI?

The Anti-AI Hedge: Apple Doesn’t Blink When NVDA Does

Bond Vol Explodes - Will SPX Notice?

European Banks Break Out: Powerful Squeeze, But Margins Whisper Caution

Revisiting Our Old Love With Obesity

Gridlock Stock And Two Smoking Barrels

The Wrap: Perfection Prevails - Shorts Maxed, Gold Wakes, Buybacks Blaze

Upside Pain: Shorts Built, Calls Burned, Dealers Flip

Gold Wakes Up: Big Sellers Flushed Out in the Puke

The AI Cartel: Miss Market, McKinsey & Goldman All In

When Everyone Believes the Same Story

Europe hums on a low-vol track

Teen Growth and the Double Club

Hammer Time: Friday’s Fear Flush May Have Marked the Low

Miss Market’s Mood, in 18 Charts

The Wrap: Suddenly Oversold, Shorted, and Systematically Sold

Say Hello to the 50-Day — NVDA’s $650 B Flush and Vol Wakes Up

Asia’s AI Bubble Just Blinked - Spillovers Coming Fast?

The Wrap: Bubble, Buffett, and Borrowing - Tech’s Triple Threat

Make-or-Break: NVDA’s $190 Decides the Market

How Artificial Intelligence Became the Market’s Real Religion

Dare the Rare? The U.S.–China Decoupling Trade Still Underpriced

Bitcoin’s 50-Week Test - Bounce or Breakdown?

If China’s Only a Nanosecond Behind - KWEB Calls Offer Massive Upside

The Wrap: Fearless Market, Fading NVDA

Cisco Was the Bubble. Nvidia Is the Market.

10-Year Breaks Out - MOVE Still Fearless

The Fearless Sell-Off: No Panic, Just Pain

EEM - Dollar Bid Wrecks the Tech Proxy Trade

The Wrap: Everything’s Stretched — Fear High, Valuations Higher, Downside Convexity Explosive

Gold on the Edge - $3900 or Bust

The Wrap: Somebody’s Gotta Pay for the AI Party

Mag7: The First Sell Signal in a Year

Boring BTC – The Magic’s Dead

When NVDA Looks "Poor" – The Real AI Mania Has Moved East

Let Them Eat LLMs

Are We Running Out of Equities?

Are We Running Out of Equities?

Positioning and the MAG7 Right-Tail Panic

Europe: The Trade Everyone Forgot, Still Winning

Goldman hedge fund honcho: "The current setup is admittedly demanding"

The Last Time Tech Looked This “Can’t-Lose,” It Did

The Wrap: Everyone’s Bullish the MAGs — What Could Go Wrong?

EEM – Weak Dollar? Think Again

TLT Trouble? — Calm Volatility Meets Inflation Fear

Dollar – The Cross That Matters

The Wrap: MAG Reversal - Too Much, Too Fast?

Super Tech, Super Stretched – Right Tail Gone Wild

The Gold Puke Pause

The MOVE Massacre

Berkshire’s Crossroads: The Oracle’s Old Economy Meets the Age of AI

The Holy Grail of Cancer — or Just Another Market Cult?

The Wrap: Fed Cut FOMO – Spot Up, Vol Up

Forced To Buy: AI Mania Goes Parabolic

$5 Trillion Beast – NVDA Eats the Industrials

The Wrap: FOMO Froth – Right Tail On Fire

Don’t Fight Retail: They’ve Poured In Nearly $300BN Since April

The Precious Puke – Levels To Watch

Small Business America Is Quietly Bleeding Out

Wall Street’s Great Emotionless Drift

After a Decade of Despair, Europe Rediscovers Its Pulse

The Wrap: Magic MAGs, Gamma Gaps & Fearful FOMO

Silver’s Puke - Chased Calls, Crushed Dreams

The Great Gold Crash

The Most Stretched Market on Earth

Post-Power Talks: Dragon’s Back, Techs on Fire

Fab Five Fundamentals

Too Pessimistic? Mag7’s Low Bar and Rising Right-Tail Risk

The Wrap: AI ATH - Climbing the Wall of Worry, Fueled by Fear

AI Euphoria Reloaded - Imagine We Go Full 1999

Gold: If This Is the Bounce — Imagine the Next Leg Down

The Other AI Superpower — China’s Innovation Bull Is Back

The Wrap: Market Still Stuck, Ready to Explode – Upside Pain Next?

Remember Oil? - The Shorts Sure Do

Gold – Healthy Reset or Just Overcrowded?

The Wrap: Range-Bound & Restless — Vols Bid, Momentum Cracks and Bubbly AI

Precious Levels To Watch

Déjà Vu: The 2006 Gold Surge Ended With a 30% Crash

Gold: If There Were Signs… Well, There They Were

The Wrap: Everything Is Weird — From Precious Puke to AI Fatigue

Silver’s Melt-Up Meets Gravity - The Party’s Over

Enough Is Enough - Gold’s Euphoria Turns Dangerous

The Wrap: They Puked the Low, Now It’s Melt-Up Mode

Upside Panic Reloaded: Gold Monthly RSI Hits 93!

Santa’s Coming - And “They” Just Shorted the Lows

Fab Five Fundamentals

Wall Street Acted Like It’s a 10% Sell-Off

A Golden Madoff? Sharpe of 4 - a level usually reserved for financial fiction

The Wrap: Can’t Keep Bulls Down

Gold Mania - Everyone’s In, What Could Go Wrong?

3 Charts On The Recent Volatility Explosion

SVB 2.0? SPX’s 50-Day Breaks as Vol Erupts

The Wrap: Welcome to Extreme Fear

Liberation Day Panic Vibes - VVIX Back at Chaos Levels

Mission Accomplished? Gold Just Did in Weeks What Took Months

3 Bond Vol Charts We Are Watching

From Guns to Gucci - The Defense Trade Unwinds

AI High Turns Into Hangover? Capex Cools And Clicks Fall

The Wrap: Parabolic Gold, Stuck Mag 7, and Stressed VVIX

Europe’s Longevity Time Bomb: The Pension Ponzi Nobody Wants to Talk About

Can’t Put a Good Man Down: Volatility Refuses to Die

The Magnificent Stuck

Gold More Overbought Than the 1980 Upside Panic

The Wrap: Fragile Calm - Stress Stays Fearful

Russell Ripping - Perfect Shakeout, Monster Rebound

3 Fear Charts We Are Watching

China Tech Cracks

Fragile Markets - Friday’s Shock Still Haunts the VIX

The Wrap: TACO Trade Tested, Metals on Fire

Fab Five Fundamentals: We are so back

SPX on Thin Ice - Must Hold Soon or 100-Day Comes Fast

Broken Markets: Silver Volatility Goes Vertical as Pure Panic Kicks In

Flows on Fire: $26B Rush Into Gold ETFs

Climbing The Wall Of Worry In Europe

My 13 year old daughter went all-in on BTC Thursday

Fear Reignited — Equities Break Key Supports, Credit Cracks, Vol Surges

The Wrap: Here We Go — Volatility Monster Awakens, Leverage Bites, Bulls Bleed

Credit Cracking - HYG Sends a Warning Shot

China’s Magic Fades — Fast Money, Falling Stars & Fugazi Breakouts

The Wrap

Precious Metals — Momentum Junkies About to Get Burned?

Vol Surge = Reversal Signal? Gold & Silver Options Flash Warning Signs

King Dollar Awakens: Big Squeeze Above 99?

Have No Fear, There’s No Bubble, Says Sell-Side

The Wrap: Nothing Is Impossible — AI Mania, Gold Roars, Palladium Breaks Out

Palladium's Power Break Out

NDX vs 1999 — Can the AI Frenzy Go Full Nuclear?

Can’t Keep Gold Down: RSI Screaming, 200-Day Left in the Dust

The Wrap: Bulls Keep Dancing, But Momentum’s Fading

Calls Gone Wild: Bullish Bets Near Record Highs

King Dollar Awakens? Gaps, Shorts & Seasonality Collide

The Wrap: Kamikaze Yields, Gold Roars, SOX Melts Up

Sexy SOX: Overbought, Overloved, Overheating?

Bondquake in Tokyo

Fab Five Fundamentals

A Meloni Market

Gold Loves Tokyo’s Bondquake

Overweight - not morbidly obese

Largest Nasdaq/S&P Gap Since Dot-Com -Enjoy the Quality Melt-Up

The AI Boom That Ate the Economy

The K-Shaped Economy: Why America’s Bottom Half Is Falling Behind

Bond Vol Implodes, SPX Cheers

The Wrap: FOMO Mania Meets AI Nuclear Fever

SPX 7300+, FOMO and Melt-Up Déjà Vu

The Wrap: Calls Chased, Puts Puked, and Squeeze Manias

Bitcoin 'Undervalued' by at Least $50-60k

Unstoppable China Tech: Got KWEB?

Down Candles, Hanging Man & Shooting Star - Is Gold In Trouble?

The Wrap: Put Hate, CAPE Stretches, Metals Melt Up

Sexy Silver Surges as AI Needs Shine

Magnificent Miners Go Parabolic

Granolas: From Market Darlings to Value Play

Double Tops Loom as VIX Fragility and CTA Convexity Build

The Wrap: NVDA Smashes Resistance, FOMO Builds, Convexity Risks Loom

Gold Exhaustion? Shooting Star Flashes As RSI Screams Overbought

China Tech Breakout: BABA Leads, Sideline Cash Chases

The Wrap: Gold Roars, MOVE Snores, Upside Gets Gamma Violent

Hate the Politicians - Date the Stocks

Too Calm? Bond Volatility Dead While Gov’t Shutdown Risk Builds

Now Is the Time to Buy the Dollar

Gold’s $4K Magnet: ETFs Roar, Officials Keep Buying

Banker's Ball

Fab Five Fundamentals

The 10 charts you need to know this Monday morning

Is it too early to start talking about a year-end melt-up?

The Wall Of Worry: Melt-Up Now, Capital Destruction Later?

Soggy BTC: Nearing The 200-Day - Should The Market Listen?

The Wrap: Breakouts, Bruised Bets and Bubbles

So Far, Just a Dip – Or the Start of Something Bigger?

Parabolic Silver: Froth Meets FOMO

Who Needs AI When You Can Have Defense?

The Wrap: Can’t Put a Good Market Down?

Dollar Trap: Specs Short, Squeeze Brewing

BABA Boom Meets China’s AI Fever

Tiny Tech Bubble Vibes: Nothing Impossible, Right?

Nobody’s Hedged For Real Gold Panic

Big Pain In Small Caps

Euphoria Kicks In: Momentum vs SPX Looks Like 2020 All Over Again

3 Silver Charts We Are Watching

Gold: Another Day, Another ATH...Specs Still Don’t Get It

We Have Heard That Stocks Can Also Trade Down

Big Trouble in Little China

Fab Five Fundamentals

Retail Army Goes Parabolic: 10 Straight Green Days and Counting

Lower every time this happened

The Wrap: Brutal Bull - Overbought Everywhere

$6,600 Gold? History Says Yes

Kill Bond Volatility: MOVE Crashes, SPX Feeds

China Bull… But Most Missed It

The Wrap: Upside Panic - Russell Rips, Most Shorted in Carnage Mode

Gold: Overbought, Overvalued, Overcrowded

Dead Brand Walking? Tesla Goes Parabolic As Fundamentals Collapse

The Wrap: Weird NASDAQ Candles, Russell at Resistance

Roaring Russell Hits Resistance

China Tech Explodes: FOMO Next

Achtung: DAX Cracks Below Range

EM Mania Now, Mean Reversion Later?

The Wrap: FOMO Rally Faces the Fed

Gold into FOMC: Unstoppable, Overbought

The Wrap: Tech Buy-In Meets AI Mania

Put Seller Party: What Could Possibly Go Wrong?

Fed Cuts, Fed Fear Fuel Gold Fire

The Seven Charts Goldman's Macro Trading Team Are Watching

Fab Five Fundamentals

The drugs start to feel like they are decaf

$4,000 Gold - Conviction Buyers and the “Forever Bid”

The Wrap: AI Euphoria Meets Put Hate

AI Bubble Hype? Credit Says No

Decade of Pain, But Will Small Caps Bite Back?

3 Bond Volatility Crash Charts That Matter

AI Can’t Run Without Silver

All This Bull, Sentiment Still Stuck

Blocked – Bitcoin’s Back Door Slammed Shut

Speculation Runs Hot, China Can’t Cool Down

Swipe Now, Moon Later: Has Sweden produced a new Spotify:esque stock darling?

The Wrap: Beyond AI - Downside Convexity, Buybacks Rolling Over

No AI, No Alpha

Asian Tech Breaking Out Everywhere

The Wrap: Divergences Flash Red, China Tech Breaks Out

Generals Don’t Lie: Last Time, SPX Sold Off

China Tech: Is This The Breakout Moment?

Mighty Russell: Years of Pain, Now Payback?

Lumberrrr Crash — 3 Charts We’re Watching

The Wrap: Inverse Fear – Cheap Puts on the Tape

Fab Five Fundamentals

Gold Goes Parabolic as Fed’s Credibility Burns

Is the Narrowness a Feature or a Bug?

Where Are We on That European Tactical Long Trade?

The Rich Hate Cash, Retail Army Loves Tech

The Wrap: NVDA Crashes, VIX Seasonality Hits - Can Markets Stay Immune?

Gold's Gamma Squeeze Is ON

You Can’t Put This Bull Down — China Roars Back

The Wrap: $1.5Bn Daily Buyback Bid Vanishes Just As Bond Vol Explodes

If only there were signs...

China’s Market “Exponentialism” Just Got Halted

The MOVE Index Just Screamed a Warning. Did You Hear It?

The Wrap: Overbought Gold, Oversold NVDA — Two Giants at Extremes

Contagion Live: JGB Explosion Fuels Volatility, Gold Surge

Contagion Live: JGB Explosion Fuels Volatility, Gold Surge

The Wrap: SPX Breaks Down, NVDA Cracks $170

Gold Breakout Goes Relentless

VVIX Screams Risk — Crowd Still Short VIX

China’s All-In FOMO

Rising Yields, Rising Fear: Bond Vigilantes Return

Comfortably worst

CTAs Maxed Out Again at 100th Percentile and Would Have to Sell >$70bn Over the Next Month in a Down-Tape

From First To Worst

Fab Five Fundamentals: Follow The Money

3,451 Cracker Barrels

The Wrap: BTC Cracks First — Tech To Follow?

China Flows on Fire – Shorts Burning

EU Luxury: From China Proxy to Catch-Up Play

The Wrap: NVDA Stalls, China AI Soars, Gold Loads

Gold – Specs Sold, CTAs Forced to Chase

Russell's Revenge

China’s AI Bubble Goes Full Mania

Missing expectations for the first time

Keep Dancing… Until Yields Break It

Shorts and Sceptics Fuel the Russell Squeeze

VIX Shorts at Extremes – Crash Risk Rising

The Wrap: Can’t Put Russell or Gold Down

Gold – Tic, Tic, Boom

Dollar Death Cross – And Then We Ripped

China Roars, Bitcoin Snores, JGBs Soar

Managements voting with their shareholder's money

China: Mother of Breakouts, King of AI

The Bullish Ph.D Says Time to Take a Breather

Where are the bulls?

The "things can only get less worse" long trade in Europe

Do Or Die For Healthcare

If you see a bubble, ride it...

Better than Tech

Please mind the gap between the AI hype and reality

Everyone Short Russell… What Could Go Wrong?

Shanghai Squeeze – Upside Panic On

Emerging Markets: Travel & Arrive

The Wrap: AI Bubble = VIX Time Bomb

The Risk Everyone’s Missing

Greed and Fear on Steroids

The Kanye–Chamath Top

The $4,000 Gold Dream: One Peace Deal Away from a Putin Punch

Too Much, Too Fast: Panic or Buy the Dip?

AI Won't Die Overnight

Gold Ready to Explode? Fear Says Yes, Cheap Volatility Is the Trade

Shanghai Roars, China Tech Snores — The Laggard Trade?

NVDA Cracks, AI Smacked, Tech Attacked

AI Mania, CAPEX Boom, and Mega-Cap Concentration — Too Big to Fail or Too Big to Fall?

Retail Chasing, Pros Fading, Crypto Wobbles, Edge to Hedge

Calm Before the Storm? Vol Bargains, VVIX Screams, Seasonality Looms

"We see immense value in owning hedges thru the rest of summer"

Russell earnings revisions breaking out for the first time in 3 years

Semis eating software

The bull is on ketamine

Fab Five Fundamentals

Market – Rich, Stretched, and Crowding Fast

ETH Fever: FOMO, Treasuries Buying, and $25K Price Targets

Tech at Dot-Com Extremes, Retail Roars, Skew Screams, and Cash is Gone

EM Mania – AI Eats Commodities, EM Prints It

UAL Soars as Premium Carriers Tighten Their Grip

Nasdaq Tops Dot-Com Era in Historic Valuation Surge

Russell Roars and Pain Trade Risk Builds

AI CAPEX Mania – Tech Titans Outspend the Rest of the Market 2-to-1

3 Silver Charts We Are Watching

2020 Vibes – Bare Positioning, Brutal Upside Risk

Russell Shorts Roasted, NASDAQ Boasted, VIX Ghosted

Europe’s Defense Bubble Runs Out of Bullets

Hedge Funds Slash Risk, Torch Russell, as Buybacks Go Brrr

ETH Mania Meets Corporate Hoarding — Stash Could Surge 10x

ChatGPT kicking those 30-year olds back into mom's basement

Mediterranean Melt-Up

The Flow To Know

Fab Five Fundamentals

So many doughnuts

Apple’s Back, Chat Is King, Fear Is Dead